Sustainable Aviation Fuel (SAF): How can European aviation decarbonize without relying on Asia?

Aviation is one of the hardest sectors to decarbonize:

- Global air traffic is projected to double by 2050, which will offset any CO2 emission reductions gained from technological improvement (ex: engine efficiency) or operational levers

- Alternative fuel options, such as electric and hydrogen, are highly limited due to weight constraints

Consequently, SAF emerges as the main option to decarbonize aviation. While SAF consumption is gaining traction due to airline commitments and regulations (e.g., ReFuelEU Aviation, in force in Europe since January 2025), its share remains minor (e.g., 1.25% for Air France-KLM), and scaling up presents significant challenges:

- Developing mature technologies to achieve production costs that result in a viable economic equation: current production costs are 2 to 5 times that of fossil jet fuel

- Ensuring feedstock availability to avoid reliance on imports from Asia: In Europe most SAF is currently produced via the HEFA process (Hydrotreated Esters and Fatty Acid), utilizing UCO (Used Cooking Oil), which is mostly imported from Asia.

Developing SAF production capacities will require massive investment.

The groundwork to catalyze SAF production investment is in place: commitments to net-zero emissions by 2050, SAF mandates in several countries and long-term offtake contracts between airlines and SAF suppliers.

However the coming five years will be crucial to turn early initiatives into operational projects, to mature the technology, reduce the production costs and develop a local feedstock supply chain. This will allow the shift towards SAF to become a national strategic advantage rather than relying on imported used oil from Asia.

1. Sustainable Aviation Fuel (SAF) is an essential lever for decarbonizing a growing aviation sector

Considering the continuous growth of air traffic and the limited potential of other alternative fuels, switching to SAF is unavoidable for decarbonizing aviation.

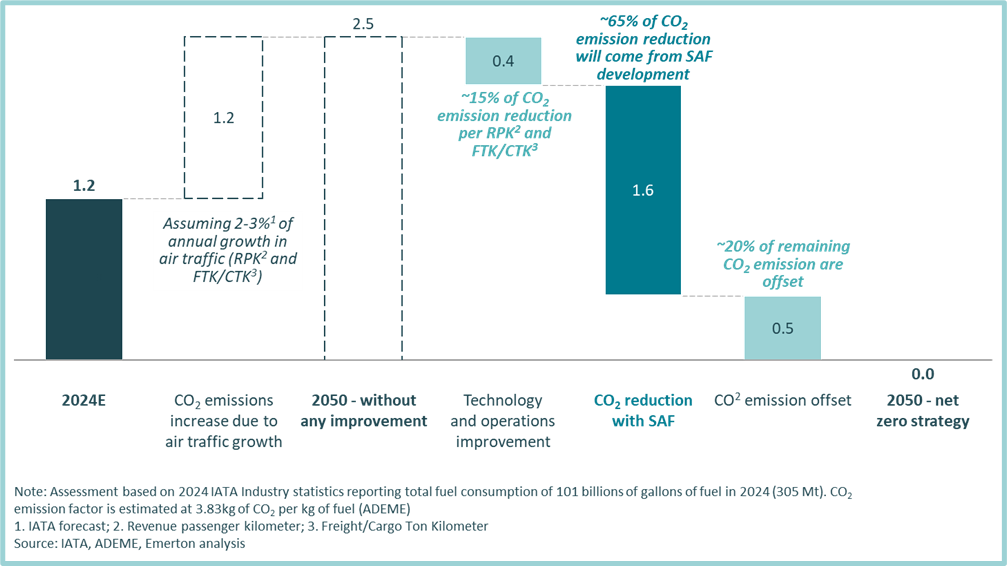

In 2024, aviation accounted for approximately 1.2 billion tons of CO2 emissions (~2.5% of global CO2 emissions). However, due to continuous air traffic growth, this sector could become a much larger contributor if transformative measures are not adopted.

The aviation sector is facing immense challenges to meet its commitment to achieve net-zero by 2050:

• Technology (e.g. new engine technologies) and operational improvements (e.g. green taxiing) will reduce CO2 emissions, but the identified levers have potential to reduce CO2 emissions by only ~15%. This reduction will be completely nullified by air traffic growth, that is expected to double by 2050

• Switching to low-carbon fuels is thus a mandatory step to decarbonize aviation and meet net-zero targets by 2050. IATA targets ~65% of CO2 emissions reduction due to the switch to low-carbon fuels.

• The remaining ~20% of CO2 emissions from the aviation sector will have to be offset (through reforestation projects for instance)

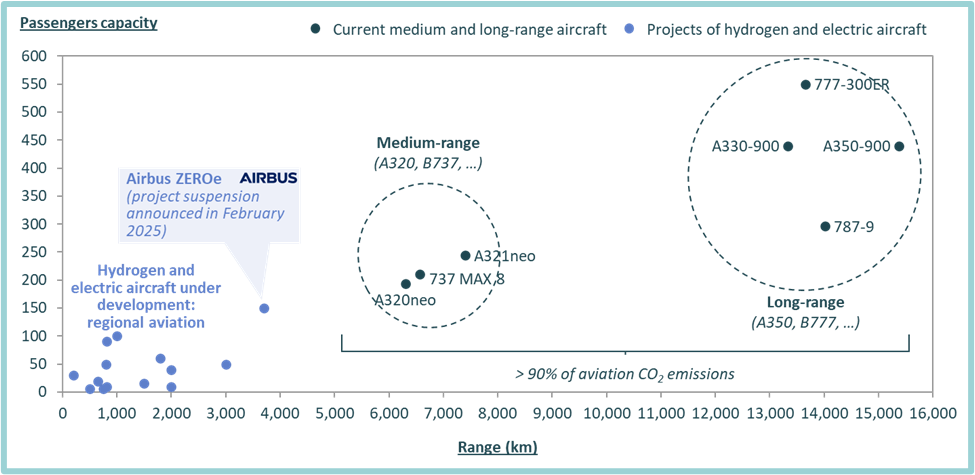

In terms of low-carbon fuel options, electricity is to date limited to small/regional aircraft due to battery weight.

Hydrogen has often been cited as a future alternative for decarbonizing aviation. However, its use as a direct fuel is constrained by technological (storage), infrastructure, and energy density limitations. Thus, current projects focus on small/regional aircraft as well.

- In 2022, Airbus launched a differentiated project (ZEROe) targeting an aircraft with more than 100 passengers and a range up to 3700km by 2035

- But Airbus recently scaled back its hydrogen-powered aircraft ambitions

Thus, among available options, Sustainable Aviation Fuel (SAF) stands out as the most viable strategy for decarbonizing aviation.

2. SAF consumption is emerging with airline commitments and regulations

Airlines are already incorporating SAF in their fuel mix and regulations like ReFuelEU Aviation (which came into force since January 2025) will secure a growing demand for SAF.

Sustainable Aviation Fuel (SAF) is jet fuel produced from biomass or synthesized from renewable hydrogen (e-fuels) and captured CO2.

Its primary advantage is compatibility with existing engines and infrastructure, allowing for a drop-in replacement of fossil kerosene.

Also, the technology has been proven in commercial flights: Apart from a few flight tests conducted with 100% of SAF, many Airlines have started to incorporate a growing share of SAF (even if it is still very low) in their fuel mix.

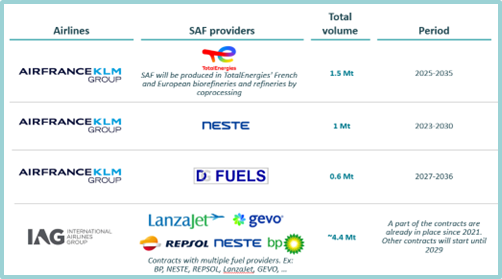

For instance, Air France-KLM and IAG have already signed partnerships with SAF producers to secure SAF supply until 2030 and target 10% of SAF in their fuel mix by 2030 (which is greater than the 6% obligation from ReFuelEU Aviation):

- Air France-KLM reported 1.25% of SAF in their fuel mix in 2024 and signed several long-term offtake contracts with SAF producers (e.g. Engie, EDF, Elyse Energy, TotalEnergies, OMV, Raven, SAF+). Notably, the agreement with TotalEnergies represents 1.5Mt of SAF between 2025 and 2035.

- IAG reported 1.9% of SAF in their fuel mix in 2024. They signed long-term offtake contracts with SAF producers like BP, Neste, Repsol, LanzaJet, Gevo and have already reported more than $3.5 billion investment in future offtake.

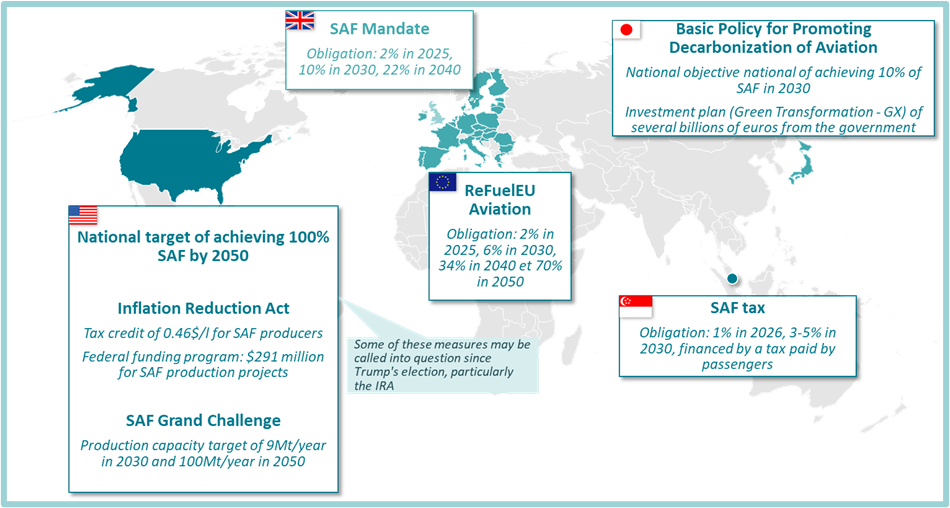

In order to boost the development of SAF, several countries have defined SAF mandates imposing progressive blending mandates on fuel suppliers and airlines:

- Europe: Since January 2025, the ReFuelEU Aviation regulation has come into force, imposing 2% of SAF in 2025, 6% in 2030 and 70% in 2050.

- UK: 2% of SAF in 2025, 10% of 2030 and for now 22% in 2040.

- Singapore has set an obligation of 1% of SAF in 2026 and is in the process of setting SAF mandates for 2030 (which are expected to be between 3% and 5%).

- Japan established a national objective of achieving 10% of SAF in 2030.

- USA has been very ambitious regarding SAF, with a national target of achieving 100% by 2050. The USA has also set strong financial mechanisms to support SAF production, especially with the Inflation Reduction Act (IRA), to target a SAF production capacity of 9Mt/y in 2030 and 100Mt/y in 2050. The recent election of Donald Trump has, of course, put this trajectory at risk, with several measures from his administration aimed at freezing climate-related funding, including provisions under the Inflation Reduction Act (IRA).

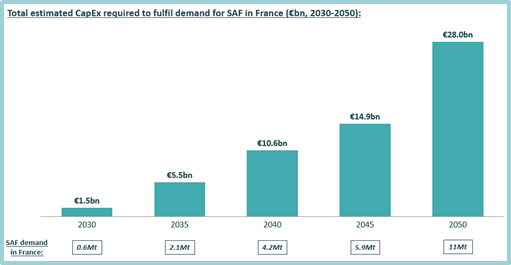

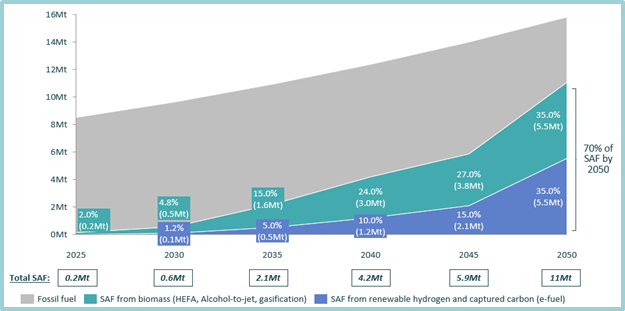

SAF mandates are essential to ensure a secured demand trajectory and stimulate investment. For instance, in France, the ReFuelEU Aviation initiative will establish a predictable SAF demand, growing from approximately 0.2 Mt in 2025 to around 11 Mt by 2050.

3. First challenge to scale-up SAF production capacities is to reduce production costs, to have a viable economic equation

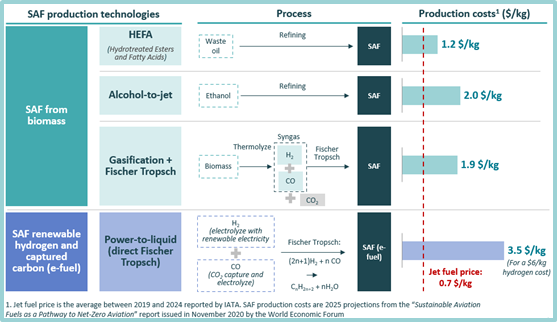

Future SAF technologies fall into two broad categories:

i. Biomass-based pathways:

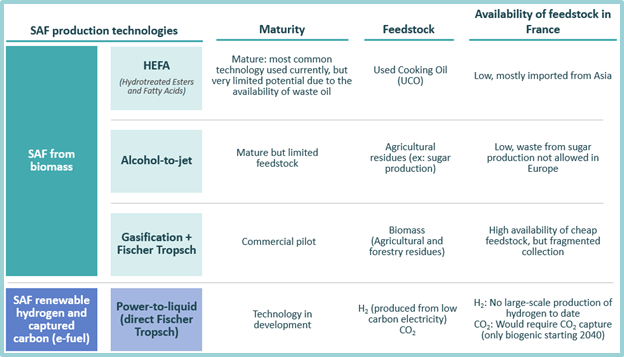

- HEFA (Hydrotreated Esters and Fatty Acids): the most mature technology, which consists of refining Used Cooking Oil (UCO). The refining process has the advantage of requiring limited investment to convert current refineries

- Alcohol-to-jet: while technologically viable, regulatory constraints on agricultural feedstocks mean local production is limited in Europe. Europe is thus expected to import SAF from Brazil for instance

- Gasification (e.g. process patented from Haffner Energy): this pathway can use a variety of biomass sources and is feedstock-agnostic. However, it generates CO2 as a by-product, which must be captured or offset.

ii. E-fuels using Fischer-Tropsch synthesis: these rely on low-carbon hydrogen and CO2. It requires vast amounts of renewable electricity to produce hydrogen and infrastructure to capture CO2 and infrastructures to transport both hydrogen and CO2.

Technology maturity and feedstock availability represent strong barriers to SAF production today. The first barrier is the production cost: even HEFA, which is the most mature technology, is twice as expensive (~1.2 $/kg) as the current jet fuel price (~0.7 $/kg in average between 2019 and 2024). The ratio can even be greater than 4 for the Power-to-liquid process (depending on electricity price).

4. 2nd challenge is the availability of domestic feedstock, to avoid reliance on imports. To date, France mainly produces SAF from UCO imported from Asia

HEFA is currently the most used process in France (and in the world), but it uses Used Cooking Oil (UCO), mostly imported (Europe imports ~80% of the UCO used) from China (~50% of total UCO imports).

Due to the lowest cost and higher level of maturity, almost all SAF produced in the world is with HEFA process. HEFA seems to be an attractive solution, but the potential is strongly limited due to the feedstock: Used Cooking Oil (UCO).

Indeed, UCO production and collection are very limited. In France, ~90kt is used per year. Even if it were to be used to produce SAF (it is also used to produce biofuels for road transportation), the volume would be negligible compared to the national demand for SAF: 0.2Mt in 2025 and 11Mt in 2050.

Thus, if the other technologies (Alcohol-to-jet, Gasification, Power-to-liquid) are not developed at an economic cost, France will have to continue to rely strongly on imports of UCO from Asia to produce SAF (which obviously limits the effect on the decarbonization of aviation).

5. The groundwork to catalyze SAF production investment is in place, but the coming five years will be crucial to turn early initiatives into operational projects

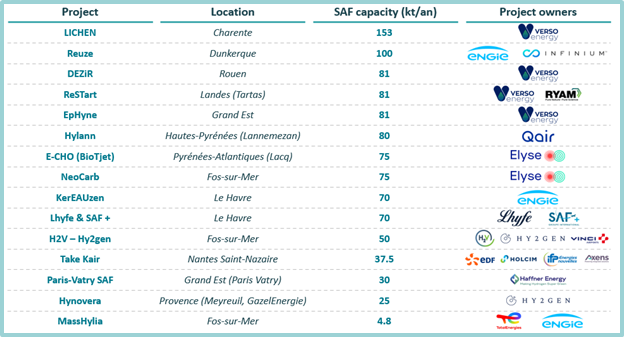

To date, ~15 projects of SAF production based on these other technologies are reported in France. They represent a total SAF production capacity of ~1Mt per year by 2030 (which is greater than the need of 0.6 Mt per year to comply with ReFuelEU Aviation).

But these projects will require massive financial investments: typical SAF production projects require more than €1 billion investment.

In total, France will need to invest around €28 billion by 2050 to build the 11 Mt of SAF production capacity required under ReFuelEU Aviation.

The groundwork to catalyse SAF production investment is in place:

- The international aviation industry has recognized the imperative to decarbonize and committed to reach net-zero emissions by 2050

- SAF stands out as the most viable strategy for decarbonizing aviation

- Many countries have defined SAF mandates, which secures a predictable and growing SAF demand

Many airlines are starting to contract long-term offtake agreements with SAF suppliers (see examples from Air-France KLM and IAG on Exhibit 10), in order to secure SAF volumes up to 2030-2035, which is a very positive signal.

However, investment from infrastructure funds remains limited to date, with Hy24 and Mirova among the first in France: in 2024, they announced a €120m investment to support Elyse Energy’s SAF production projects in France (and Spain).

The next five years will be critical for the successful implementation of the ~15 SAF projects planned in France. Key priorities include:

- maturing the technology

- reducing production costs and demonstrating a viable business model

- developing a local feedstock supply chain. This will allow the shift towards SAF to become a national strategic advantage, rather than relying on used oil import from Asia

This transition to SAF also creates an opportunity for new entrants to challenge historical players (ex: TotalEnergies, BP, ExxonMobil):

- Companies from the hydrogen sector entering the field, such as Elyse Energy, H2V, Lhyfe, and Hy2gen,

- Technology providers like Haffner Energy,

- Major energy players like Engie seizing this opportunity to enter the emerging green fuels market.